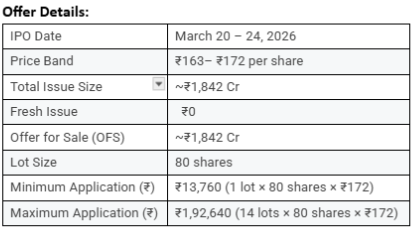

Central Mine Planning & Design Institute Limited (CMPDI) IPO: Here's What You Need to Know! A deep-dive into India's government-backed mining consultancy company making its stock market debut The IPO season continues, and this time it's a nameclosely tied to India's coalbackbone. Central Mine Planning & Design Institute Limited (CMPDI), a wholly owned subsidiary of Coal India Limited, has opened its subscription window from March 20–24, 2026. Let's break it down simply. Offer Details and Funds Utilization Funds Utilization Since this is a 100% OFS, the company receives no proceeds. All funds go directly to the selling shareholder, Coal India Limited. The purpose of this IPO is simply to list CMPDI on BSE and NSE.

Company Profile and Business Model Think of CMPDI as the brain behind Coal India's mining operations. Founded in 1975 and headquartered in Ranchi, Jharkhand, it operates as a specialised consultancy arm providing end-to-end technical services to the coal sector. Its service verticals include coal exploration and mine planning, environmental engineering, coal beneficiation, IT and communication services, human resource development, and remote sensing and field services. The company also serves clients outside the CIL group, including the Ministry of Coal and other government agencies, which contributed ~34% of revenue in 9M FY26 — up from just 17.3% in FY23, showing meaningful diversification.

Industry Overview and Outlook India's coal story remains large and long. A few key data points worth noting: coal-based thermal power plants account for ~73% of India's electricity generation as of FY25, and coal demand in India is expected to grow at a CAGR of 3.7% between FY25 and FY30. CIL alone operates 313 mines and accounts for 74% of domestic coal supply. As long as India's energy needs keep growing, the demand for mine planning and consultancy services tied to the coal sector remains structurally supported. That said, global ESG pressures and India's renewable energy push could gradually temper the long-term outlook for coal-linked businesses.

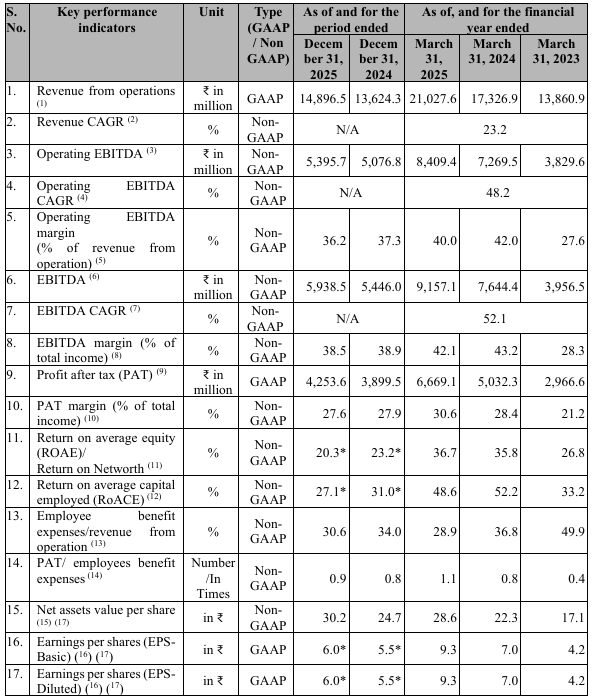

Financial Performance The numbers from the RHP tell a compelling growth story: Revenue CAGR (FY23–FY25) 23.2%: steady compounding growth backed by a captive client base. What really stands out here though is the quality of earnings. An EBITDA CAGR of 52.1% and an Operating EBITDA CAGR of 48.2% over the same period show that profitability has grown significantly faster than revenues, meaning the company is becoming more efficient as it scales. PAT margins have consistently stayed in the 21–31% range, which is exceptional for a services business. The 9M FY26 numbers (PAT of ₹425 Cr in just nine months) suggest FY26 could comfortably surpass FY25 on an annualised basis. ROAE stands at a healthy 36.7% for FY25, further underscoring the capital efficiency of the business. Key Risks and Concerns No IPO analysis is complete without looking at what could go wrong: 1. Extreme Client Concentration — The top 10 clients contributed 93.8% of revenue in 9M FY26 and virtually all of them are Coal India subsidiaries or Ministry of Coal entities. If CIL's business slows, CMPDI's revenue will feel it directly. 2. Parent Dependency — CMPDI operates largely on nomination-based work awarded by Coal India. It has no independent sales muscle. Any change in CIL's internal policies could directly impact CMPDI's order book. 3. Coal Sector Risk — As India gradually transitions toward renewables, long-term demand for coal consultancy services could plateau. This is a slow-moving but real structural headwind. 4. No Proceeds to the Company — Since this is a pure OFS, CMPDI gets nothing from this IPO. It is purely an exit/divestment exercise by the government through Coal India.

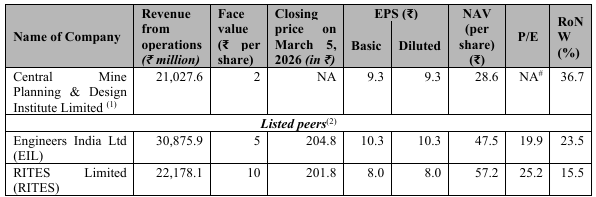

Valuation At the upper price band of ₹172 and based on FY25 EPS of ₹9.3, the implied P/E ratio works out to ~18.5x. Let's see how that stacks up against listed peers:

Since there are only two listed peers, the industry average and median are both the same at ~22.6x. Against this, CMPDI at ~18.5x is priced at a meaningful discount to both peers, which on the surface looks attractive. What makes this more compelling is that CMPDI's RoNW of 36.7% is significantly superior to both EIL (23.5%) and RITES (15.5%), suggesting the company is actually of higher quality yet is being offered cheaper. The zero-debt balance sheet and consistently expanding margins add further weight to this argument. That said, the near-total dependence on Coal India and the long-term coal sector headwinds are factors the market will watch closely post-listing.

Conclusion

CMPDI is a unique IPO, a government-backed, high-margin consultancy business with a near-monopoly on mine planning services for India's largest coal producer. The financials are genuinely impressive: 40%+ EBITDA margins, zero debt, and consistent profit growth. The flip side is an almost total dependence on Coal India, a coal sector that faces long-term ESG headwinds, and an IPO structure that benefits the seller (the government), not the company itself.

This blog is purely for educational and informational purposes and is not a buy or sell recommendation. Always do your own research and consult a SEBI-registered financial advisor before making any investment decision.