There are no items in your cart

Add More

Add More

| Item Details | Price | ||

|---|---|---|---|

A deep-dive into India's multi-service manpower company hitting the markets this week

The IPO market is buzzing again, and Innovision Limited has just opened its subscription window (March 10–12, 2026). If you've seen the name pop up and are wondering whether this one deserves your attention, you're in the right place. Let's break it all down.

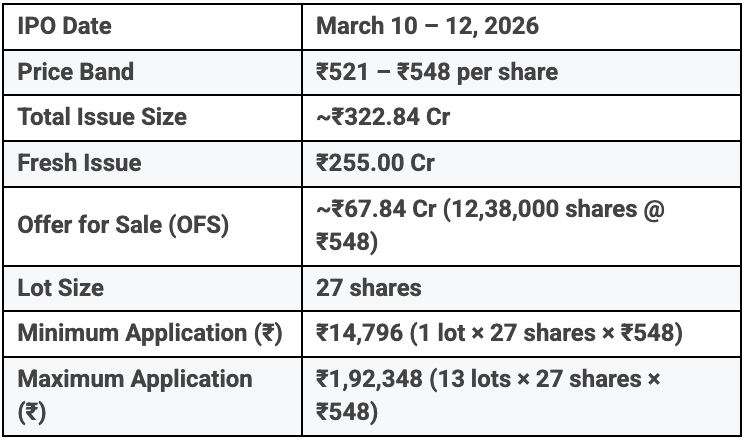

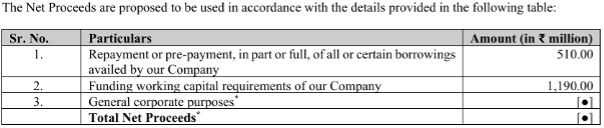

Offer Details and Funds Utilization

Offer Details:

Funds Utilization:

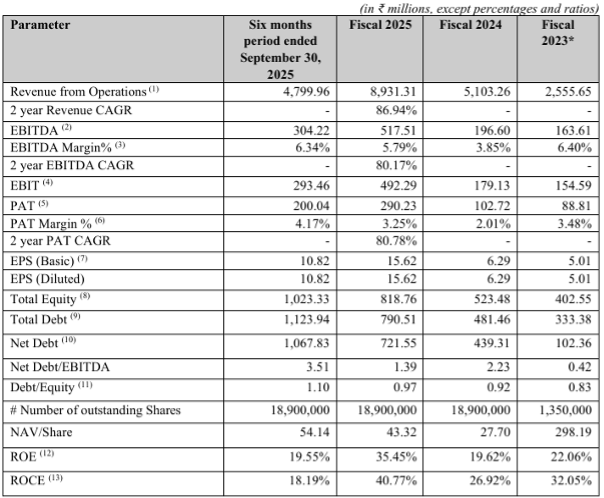

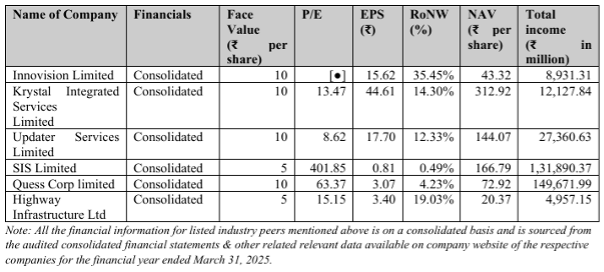

Financial Performance

Financial Performance

So here's the interesting part, against the industry average P/E of ~100x, Innovision at ~35x looks attractively priced. But the average is heavily skewed by SIS Limited's outlier P/E of 401x. A more grounded comparison is the industry median P/E of ~15x, against which Innovision's asking valuation of ~35x appears stretched.

Innovision does stand out with a notably superior RoNW of 35.45% compared to all peers, which is a genuine positive. However, with thin margins, an ongoing legal overhang, and a valuation premium over the peer median, the numbers demand careful scrutiny.

Conclusion

Innovision Limited is a multi-segment services business operating in genuinely high-growth industries. The revenue trajectory is impressive, and the company's diversification across security, manpower, tolling, and skilling gives it multiple growth levers. That said, the NHAI debarment issue is a material risk that can't be brushed aside, margins remain thin, and the asking valuation is not cheap.This blog is purely for educational and informational purposes and is not a buy or sell recommendation. Always do your own research and consult a SEBI-registered financial advisor before making any investment decision.